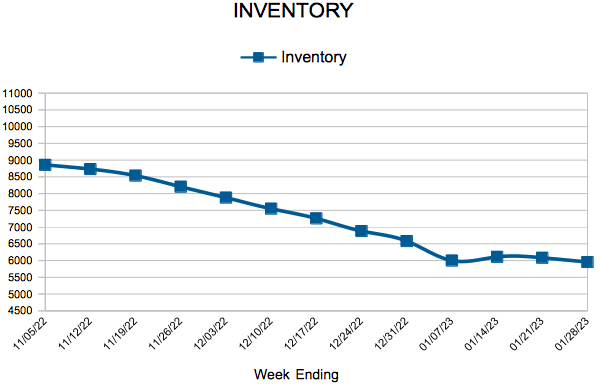

Inventory

216, Water Street,Excelsior MN 612-275-9734

For Week Ending February 11, 2023

For Week Ending February 11, 2023

Nationally, the median age of owner-occupied homes is 40 years, according to the 2021 American Community Survey (ACS), the most recent survey available. Among owner-occupied homes, nearly half were built before 1979, while only 10% of homes were built 2010 or later. As America’s housing stock continues to age, and with a limited supply of residential new construction available, the home renovation industry has experienced a boom the last few years, especially during the pandemic, which saw homeowner remodeling and repair spending increase by double digits, per the Leading Indicator of Remodeling Activity (LIRA) from the Harvard Joint Center for Housing Studies.

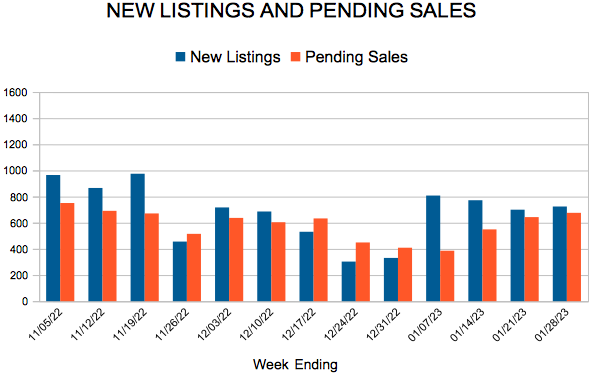

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING FEBRUARY 11:

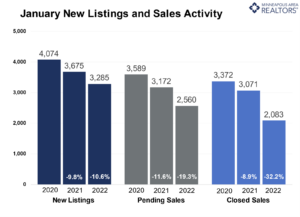

FOR THE MONTH OF JANUARY:

All comparisons are to 2022

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

February 16, 2023

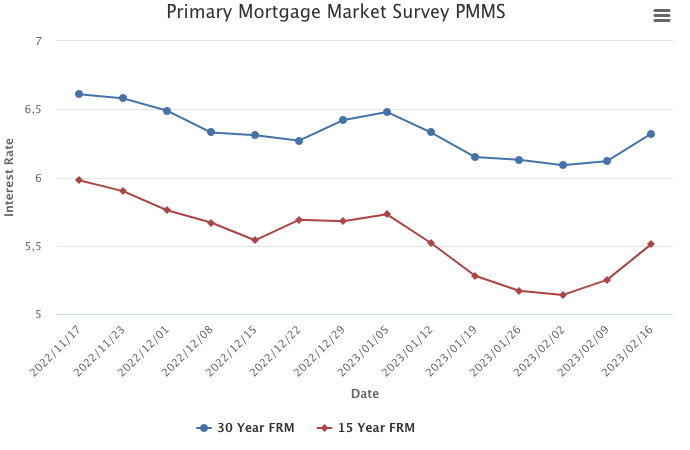

Mortgage rates moved up for the second consecutive week. The economy is showing signs of resilience, mainly due to consumer spending, and rates are increasing. Overall housing costs are also increasing and therefore impacting inflation, which continues to persist.

Information provided by Freddie Mac.

(February 15, 2022) – According to new data from Minneapolis Area REALTORS® and the Saint Paul Area Association of REALTORS®, the median sales price across the Twin Cities grew 2.7 percent to $341,995. The metro is returning to historic trends for median home price growth.

Inventory & Home Prices

The Twin Cities’ median home price grew 2.7 percent despite 19.3 percent fewer signed contracts. After about three straight years of roughly 10.0 percent year-over-year price growth, this modest increase is more aligned with the historical average of 3.2 percent across the region. While price growth is slowing, it remained positive throughout 2022 and this year is expected to continue that trend of moderating growth, barring any unforeseen circumstances.

“Anyone concerned about runaway home prices should be comforted by the more typical price growth we’re seeing, which gives buyers a chance to catch their breath and incomes a chance to catch up,” said Brianne Lawrence, President of the Saint Paul Area Association of REALTORS®. “While the Twin Cities remains a seller’s market, homes are taking longer to sell and sellers are accepting less than their list price.”

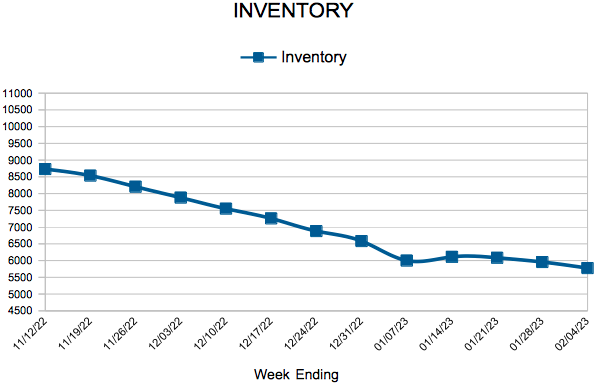

Softening buyer activity led to 14.5 percent more homes on the market at month-end, closing out January with 5,588 units in inventory. Yet we remain undersupplied—especially if interest rates moderate in response to inflation subsiding and demand once again soars. The metro only has 1.3 month’s supply of inventory. Typically 4-6 months of supply are needed to reach a balanced market.

Sales & Listings

As the market reacts to a series of aggressive rate hikes by the Federal Reserve in an effort to slow borrowing and cool an overheated economy, home buyer activity has also cooled. Facing higher mortgage rates and monthly payments than they would have in 2022, buyers signed 2,560 purchase agreements, 19.3 percent fewer than last year. Meanwhile 2,083 homes closed, down 32.2 percent from last year and the lowest figure since 2010. But that reflects contracts signed 30 to 60 days earlier.

“Sellers need to be priced right and may not see a dozen plus offers immediately, but most sellers are getting deals done with terms they’re comfortable with, and still more quickly than in the past,” according to Jerry Moscowitz, President of Minneapolis Area REALTORS®. “The truth is, what feels like a slow-down from light speed is actually close to how the market used to and probably should feel. You know, there’s actually a chance that listing you’ve been eyeing will be there later tonight or even tomorrow!”

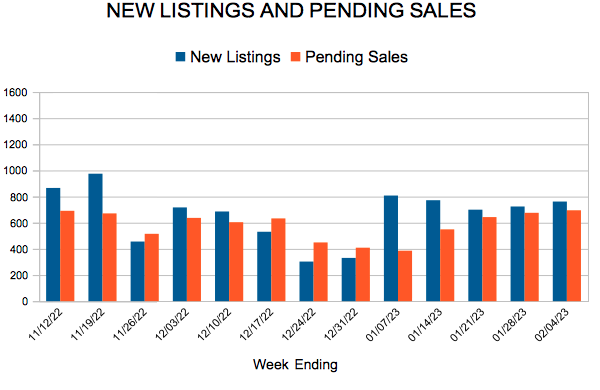

There were 3,285 homes listed in January, 10.6 percent fewer listings than January 2022. Last month, half of all sellers sold homes for at or below 97.3 percent of their list price compared to 100.0 percent last year. Additionally, they accepted those offers after an average of 60 days on market compared to 41. Today’s sellers should be patient, flexible and ensure their expectations are in-line with market realities.

Location & Property Type

Market activity varies by area, price point and property type. New home sales fell 30.8 percent while existing home sales were down 31.3 percent. Single family sales fell 33.3 percent, condo sales declined 5.7 percent and townhome sales were down 32.3 percent. Sales in Minneapolis decreased 25.8 percent while Saint Paul sales fell 40.2 percent. Cities like St. Michael, Andover, and Minnetonka saw the largest sales gains while Savage, Eagan, and Brooklyn Park all had notably lower demand than last year.

January 2022 Housing Takeaways (compared to a year ago)

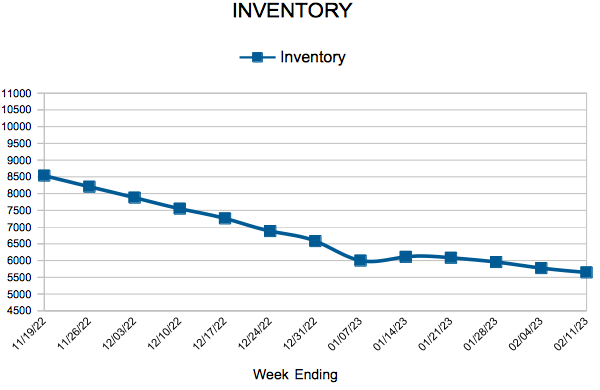

For Week Ending February 4, 2023

For Week Ending February 4, 2023

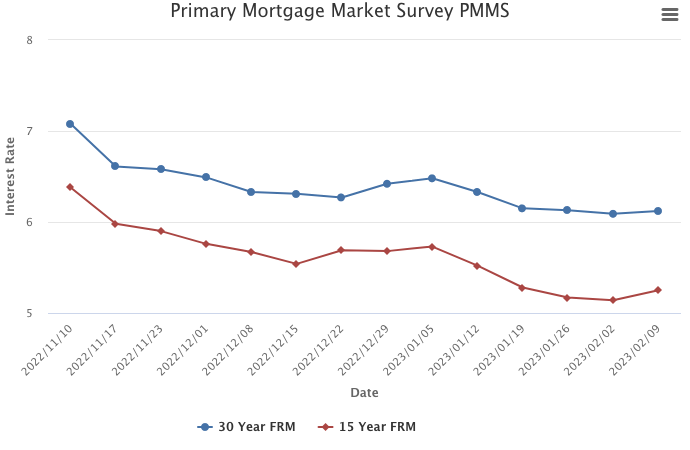

Mortgage rates continued their downward trend, with the 30-year fixed-rate mortgage averaging 6.09% the week ending 2/2/23, according to Freddie Mac. Mortgage rates have declined steadily for the past 4 weeks and are now at their lowest level since their peak in November, when rates hit 7.08%. The drop in rates could save homebuyers hundreds of dollars on their monthly mortgage payments and may provide a boost in home sales ahead of the spring selling season.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING FEBRUARY 4:

FOR THE MONTH OF DECEMBER:

All comparisons are to 2022

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

February 9, 2023

Following an interest rate hike from the Federal Reserve and a surprisingly strong jobs report, mortgage rates increased slightly this week. The 30-year fixed-rate continues to hover close to six percent, and interested homebuyers are easing their way back to the market just in time for the spring homebuying season.

Information provided by Freddie Mac.