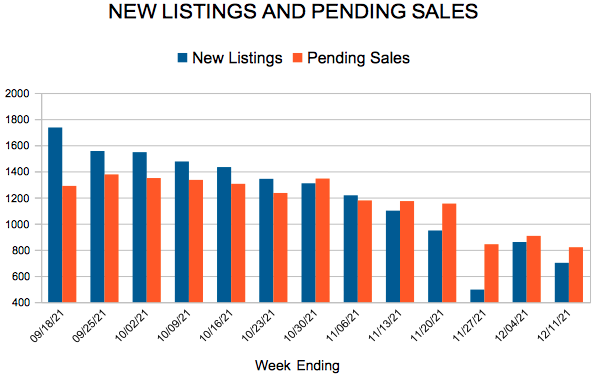

New Listings and Pending Sales

216, Water Street,Excelsior MN 612-275-9734

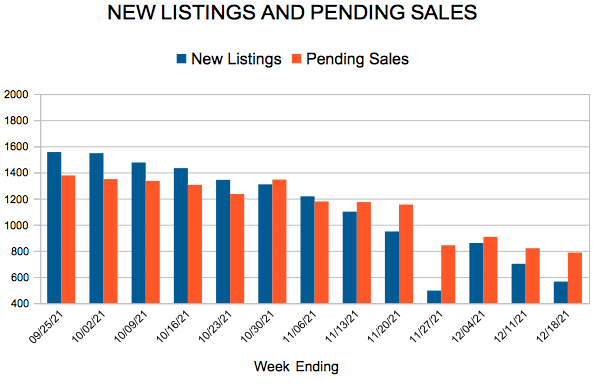

For Week Ending December 18, 2021

For Week Ending December 18, 2021

Single-family rents increased 10.9% year-over-year as of last measure, the fastest year-over-year increase in more than 16 years, and more than 3 times the rate of increase a year earlier, according to the CoreLogic Single-Family Rent Index (SFRI). Vacancy rates are at a 25-year low, as demand for rental units has surged this year due to skyrocketing sales prices and low inventory in the residential housing sector, leading some aspiring buyers to rent while waiting for the market to moderate.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING DECEMBER 18:

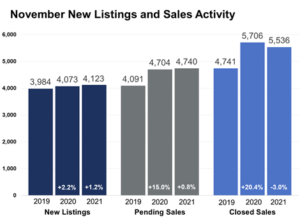

FOR THE MONTH OF NOVEMBER:

All comparisons are to 2020

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

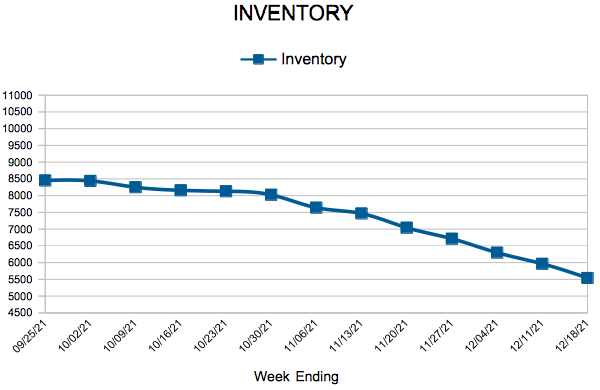

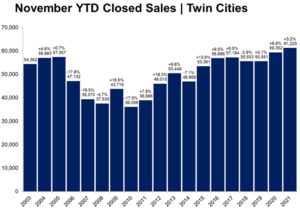

Inventory levels tumbled 18.6 percent compared to a 40.4 percent decline back in May. “While the housing shortage is still very real, there are signs that the ultra-competitive landscape is easing a bit,” according to Tracy Baglio, President of the Saint Paul Area Association of REALTORS®. “But not before we managed to post a new record for closings through November. I expect this to continue as rates remain attractive.”

Market activity varies by area, price point and property type. Home sales doubled in the Cleveland, Windom, Corcoran and Hawthorne neighborhoods, but fell over 50.0 percent in Cooper, Hale and Jordan. Sales in Falcon Heights, Delano, North Branch and Mendota Heights rose over 80.0 percent but fell over 50.0 percent in Wayzata, Medina and Wyoming. Home sales over $1M rose 43.6 percent over the last 12 months. Sales between $150,000 and 190,000 dropped 31.0 percent. Sales in Minneapolis reached their second highest level since 2005. Though a small share overall, condo sales increased more than single family and townhome units.

November 2021 by the numbers compared to a year ago

Months’ supply of inventory was down 21.4 percent since last year at 1.1 months. That’s well below the 5 months that’s considered balanced. Percent of List Price Received at Sale remained at 100.7 percent since last year.

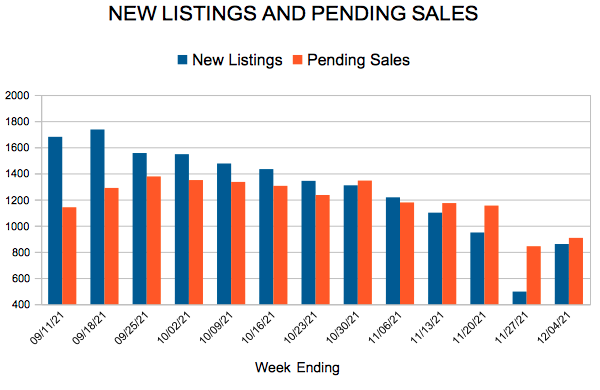

For Week Ending December 11, 2021

For Week Ending December 11, 2021

With developable lots in short supply across the country, home builders are finding other ways to meet booming buyer demand. According to the most recent Annual Builder Practices Survey, one in four new single-family detached homes built in 2020 were located in established neighborhoods, with 19% of those homes built on infill lots, while 6% were teardowns. Demand for single-family homes continues to outpace supply, and infill development is expected to increase in market share in 2022 as builders ramp up production.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING DECEMBER 11:

FOR THE MONTH OF NOVEMBER:

All comparisons are to 2020

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.